VSAC transferred the servicing of your Federal Student loans to American Education Services and the guarantee of all VSAC Federal Student loans to the Trellis Company, an approved Federal Guaranty Agency, over the weekend of March 16th. CLICK HERE for more information.

Upcoming Events

8:00am - 3:00pm Lake Morey Resort

Uncovering Curiosity: Learning for the Long Game The 19th Annual Transition and Career Planning Conference, hosted by VSAC's Vermont State GEAR UP program in partnership with HireAbility Vermont, the Vermont...

8:00am - 4:00pm daily through August 8 at CCV-Montpelier

Promoting High Quality Practices in High School Mathematics Through the Lens of EMC 2 Are you interested in offering EMC 2 in the future? If so, you should consider attending...

Student Loans with You in Mind

for undergraduate, graduate/professional students & parents

You’ve gotten your free federal aid, applied for state grants, and maybe have some scholarships set. You’ve looked at your savings, but you still come up short on what you’ll need to pay. That’s where student loans come in.

You’re not alone — 7 out of 10 families use a loan to cover some of their education expenses. Like you, we want to minimize the amount of money you’ll owe. Our nonprofit mission provides solutions that consider your current and future education dreams.

For more than 50 years, Vermont families have trusted VSAC as their source for information, counseling, financial aid, and loans to achieve their education goals.

Learn more about VSAC student loan eligibility and parent loan eligibility.

You’re not alone — 7 out of 10 families use a loan to cover some of their education expenses. Like you, we want to minimize the amount of money you’ll owe. Our nonprofit mission provides solutions that consider your current and future education dreams.

For more than 50 years, Vermont families have trusted VSAC as their source for information, counseling, financial aid, and loans to achieve their education goals.

Learn more about VSAC student loan eligibility and parent loan eligibility.

Save Money by Comparing Student Loans

Rates last pulled: April 3, 2024

You're in the right place.

VSAC offers competitive Student Loan rates.

Check an existing application.

Loan Terms

10 or 15 years

Repayment Timing

3 options:

- Pay while in school

- Pay interest only while in school

- Pay later

Discounts

0.25% interest rate discount for auto debit

Fees

- No origination fee

- No application fee

- No prepayment penalty

Cosigner Release

Yes, to qualified student loan borrowers.

Loan Terms

10 or 15 years

Repayment Timing

2 options:

- Pay while in school

- Delay payment for 12 months

Discounts

0.25% interest rate discount for auto debit

Fees

- No origination fee

- No application fee

- No prepayment penalty

Get the Money You Need

7 out of 10 families use a loan to cover education costs.

Are you new to the world of education loans?

Let VSAC be a loan resource so you can confidently make the right choices now and successfully manage your education costs down the road.

How do you really know which loan is right for you?

We’ll show you what to look for and how your choices can help reduce the amount you’ll ultimately have to repay over the life of your loan.

Why are VSAC student loans right for you?

As Vermont’s nonprofit higher education state agency, VSAC offers low-cost fixed-interest rate private loans for students and parents.

Cost-Saving Steps Before You Borrow

Here’s the key: Loans are borrowed money that must be paid back with interest. This means that the amount you repay will always be more than the amount you borrow. To minimize what you need to borrow and pay back, consider these tips:

- It's worth repeating: Take advantage of free aid first. Apply for all available grants and scholarships. This “gift aid” doesn’t have to be paid back.

- Use savings and current income. Explore tuition payment plans, which spread payments out over the academic year.

- Accept a work-study job if it's in your financial aid offer. These part-time jobs allow you to earn money toward college expenses. Or consider a part-time job while in school. Studies show that working up to 20 hours a week may actually improve your grades, since you’ll become pretty adept at time management.

- Cut expenses and economize while in school. The cardinal rule? Live like a student in school so you don't have to live like one for 10 years after graduation.

- Understand how the interest rate and the repayment plan you choose will impact your cost of borrowing.

- Borrow only what you need. Your goal should be to minimize loans as much as possible. You can choose to decline a loan or borrow less than what is offered, reducing what you’ll need to pay back.

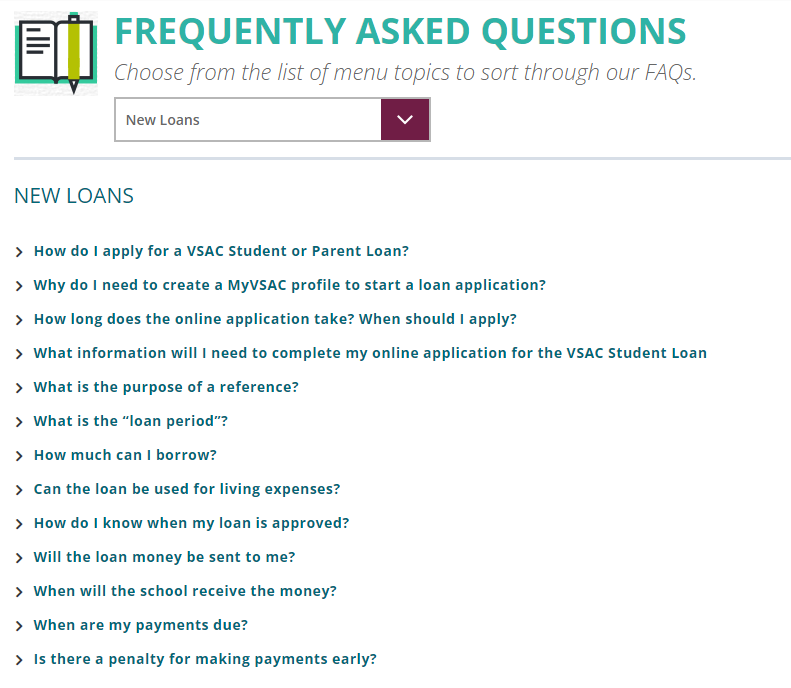

Loan FAQS

Applying For a Loan

- Who's eligible for a VSAC loan?

Vermont residents attending in and out-of-state higher education institutions, as well as students considering Vermont for higher education are VSAC loan eligible.

- How do I apply for a VSAC Student or Parent Loan?

Easily and securely apply online. Get started here.

- When should I apply?

You should apply for a VSAC loan after you've received your financial aid offer, accepted any federal loan offers, checked savings account, but still owe money toward your higher education bill.

- How long does the online application take?

It takes just a few minutes to complete the online application.

- What information will I need to complete my online application for the VSAC Student Loan or Parent Loan?

Before you start your application, be sure to grab:

- Your home address and email address

- Your date of birth

- Citizenship (Resident Alien ID # if applicable)

- Your Social Security Number

- Your driver's license state

- Estimated financial aid

- School name

- Requested loan amount & loan period (month/year of school)

- 2 references who have known you for at least 3 years and are not your parents or your cosigner

- Your cosigner's name

- Your cosigner's home and email address

- Your cosigner's phone number

- How much can I borrow?

You should only borrow what you need to cover the remaining balance on your bill. Use this formula

Cost of attendance - (Grants + Aid + Scholarships) - (Savings) = Projected loan amount.

Remember: You never have to borrow the full amount that's offered. A lot of schools offer payment plans, so getting a job or being part of a work-study program can relieve some of the unnecessary costs of a loan.

- What happens after I submit my application?

After you submit your application, VSAC will contact your school to certify your loan request.

Remember to check your registered email for important updates about your account, including notification of your Final Disclosure.

- How do credit inquiries affect my credit score?

Many people believe that if they shop around for loans, every inquiry into their credit will have a negative impact on their credit score. Not so.

While the FICO scoring formula does take student loan comparison shopping into account, loan shopping during a certain timeframe (30 days is a good rule of thumb, though this can vary), generally will have little to no effect on your credit score. With that said, it's considered good practice to do some comparison shopping before you apply.

If you’re not offered loan terms (rates & fees, for example) that you expected when you applied for a particular loan, stop your application and ask why. If it's a result of your credit score, see if there's another lender that can offer you a better rate with your score.

For a more comprehensive discussion of rate-shopping and inquiries, visit MyFico Credit Checks. Get more information and advice on how to protect your credit score at MyFico.

Loan Approval

- How do I know when my loan is approved?

Once the loan is approved, VSAC will provide the borrower with a Final Disclosure statement via email. This disclosure provides an estimated repayment schedule, loan terms, along with details about the borrower’s “Right to Cancel.”

- How soon will the funds reach my school?

Once your application is approved and all of your steps are completed, VSAC disburses funds directly to your school according to the school's disbursement calendar. Typically, one disbursement will be sent in fall, and a second in January or February.

- Can my loan be used for living expenses?

Loans can be used to cover the cost of education minus any other financial aid. Please contact your school’s financial aid office to confirm what is included in your total cost.

- Can I cancel my loan?

The Right to Cancel period begins when the loan is approved—during this time you have the option to cancel or reduce the loan amount. VSAC must wait for this period of time to end before sending money to the school. After the Right to Cancel period ends, the funds are sent to the school on the dates requested by the school.

Loan Payments

- When are my payments due?

It depends on the repayment plan that you selected on your loan application. The plan you selected determines when payments are due.

- Is there a penalty for making payments early?

No, in fact, we encourage you to make payments early on. This will guarantee you'll save money in the long run and keep the total cost of your education low.

- A new school year is starting, can I add to my existing VSAC Student or Parent Loan?

Unfortunately, you can't. A new loan is required each academic year. This can sometimes be beneficial since rates change and especially if you’ve been improving your credit score.

- Can I still apply if I don’t have a cosigner?

Every VSAC Student Loan requires a cosigner who meets VSAC’s credit criteria.

VSAC is dedicated to offering affordable loan options, and loans without a cosigner tend to have higher interest rates. Having a cosigner on your VSAC Student Loan allows us to offer you low fixed-interest rate options.

If you don’t have a cosigner and still need a loan, ask your school’s financial aid office if they can recommend a lender who doesn’t require one.

- What is my responsibility as a cosigner?

If you're a cosigner, you have a responsibility to support the student during the life of their loan. Together you both should:

- Create a financial plan for repayment

- Communicate on repayment issues (e.g. being possibly late on a payment)

- Discuss loan payments. As a cosigner, you're equally liable for the loan and expected to make payments, including any late or collection fees, if the student borrower is unable to pay on the VSAC Student Loan.

- The cosigner is also required to sign all paperwork along with the student borrower

- Research cosigner release options and make a plan to revisit these options during the life of the loan

As a cosigner, you'll also receive billing statements and the loan(s) you cosigned will appear on your credit report.

- I want to apply as a cosigner. How do I start a loan application?

Use the link in the email invitation from the student borrower to start your application online. The link will first take you to the MyVSAC login page.

If you've never used MyVSAC, click “Register Now”. After you create a MyVSAC profile, the link will take you directly to the loan application you were asked to cosign by the student borrower.

- What if my cosigner is denied?

If your cosigner is denied, you'll need to start a new loan application with a different cosigner.

- Can the cosigner be removed?

Yes, cosigner release may be available, upon request, to student borrowers who meet VSAC’s credit criteria after 48 months of active repayment.

Helpful Tools as You Borrow

FAQs for New Loans

My Education Loans Guide

VSAC Blogs

About Your Interest Rate

1Lowest APR's are available for the most creditworthy applicants, Immediate Repayment, lowest term option and include VSAC's 0.25% interest rate discount.

2APR's for student and parent borrowers assume a $10,000 loan where the student attends school for 4 years and 2 equal disbursements in the first year.

For Student and Parent Loan Immediate Repayment, loan enters repayment at final disbursement. For Student Loan Interest Only and Deferred Payment, loan enters repayment after 4 years. For Parent Loan Delayed Repayment, loan enters repayment one year following final disbursement.

To receive a 0.25% interest rate discount, the borrower must enroll in VSAC’s auto debit through LoanPay. The interest rate discount benefit is for VSAC Student, VSAC Parent, and VSAC Choice loans with credit approved on or after May 11, 2023, for the 2023–2024 loan product year. The discount applies during active repayment when you make full or agreed upon reduced payments, as long as: (1) Your monthly payment is successfully withdrawn from the authorized bank account each month; (2) All your VSAC loans are 15 days or less past due; and (3) You agree to receive paperless statements. The interest rate discount is suspended during no-pay forbearance, after 3 consecutive failed payments, or if you cancel paperless statements or auto debit. The interest rate discount will not be reflected in the credit agreement, or disclosures you receive. You must enroll in VSAC’s auto debit through LoanPay when your loan enters repayment.

VSAC reserves the right to modify, terminate, or discontinue borrower benefits at any time, at its sole discretion.