Weighing Your College Offers

If you're reading this, then you've probably applied to schools, been accepted to a few, and maybe you've started receiving financial aid offers. Once your student aid offers come in, you’ll be ready to start planning how each school will support your education or career training dreams.

VSAC knows the college decision process can be just as overwhelming as the search process. That’s why we've broken down the decision process into 3 steps:

- Understanding your financial aid offers

- Crunching the numbers

- Weighing your options & making your decision

VSAC wants you to feel confident and empowered when comparing financial aid packages. We also know that students and families want to enjoy education at the lowest cost possible. Reviewing and choosing the best offer eases the financial burdens that college can cause.

Wherever you’re at with your higher education decision process, we’ve outlined three steps to make your final decision easier.

1. Understanding your financial aid offers

College admission time is an exciting moment in life! Whether you were part of early decision or have colleges accepting you on a rolling basis, the next steps you take will have an amazing impact on your life.

After acceptance letters, financial aid offers from each school are on their way. Each offer is based on your FAFSA information, along with other forms you've been asked to submit. Each financial aid offer will be different, and each school has different financial aid policies for offering money.

There's a lot to understand, but we've made it easier by laying out some of the most important steps when you're weighing your options. Understanding your offers is the first step.

2. How to crunch the numbers

After reviewing your financial aid offers, separate grants or scholarships that don't require repayment from loans that you'll need to repay. To make comparing your offers and costs easier, we provide two ways to find your "bottom line":

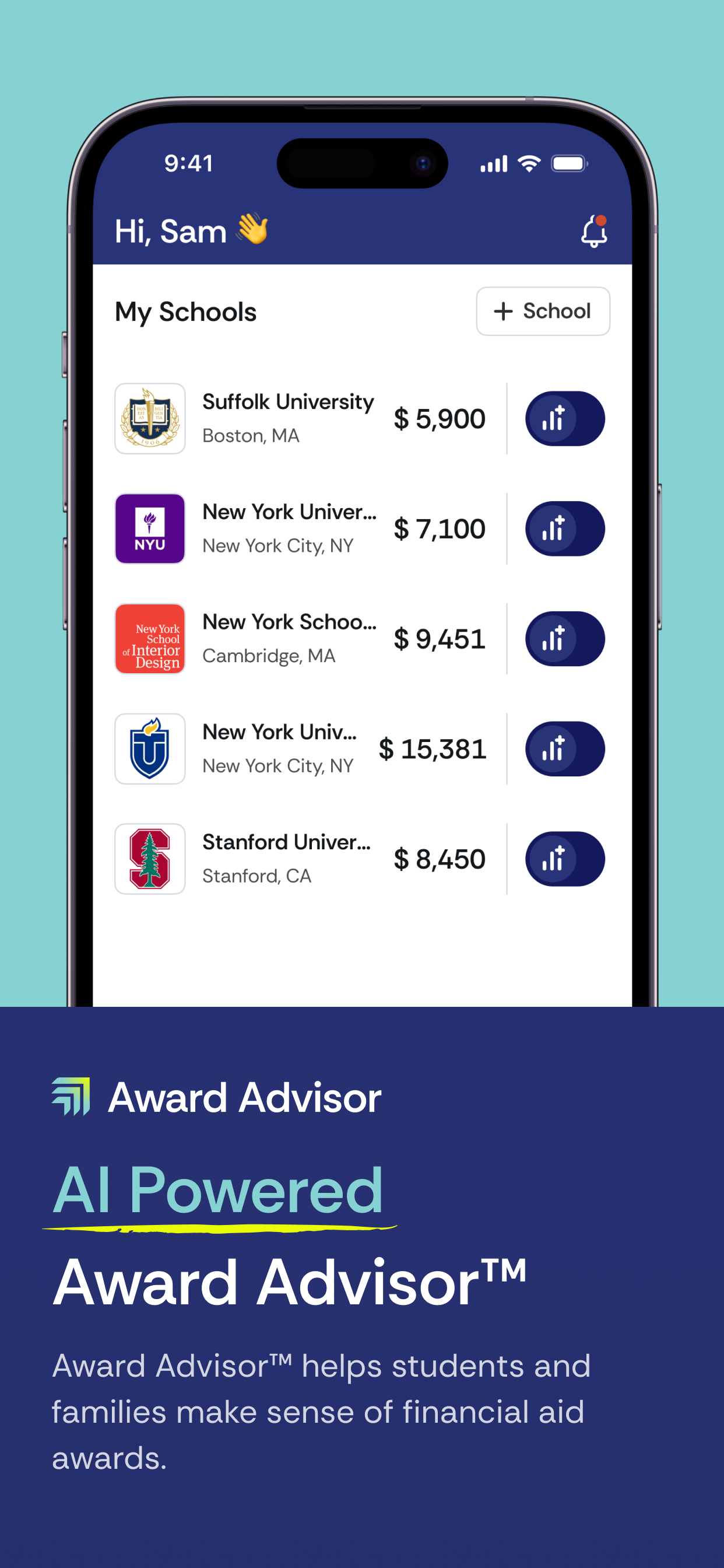

Option 1: Stop sorting through confusing financial aid letters and let Award Advisor™ provide the clarity you need. Our free app is built specifically to help students and their families:

- Add Your Schools: Start by adding the colleges you’re considering keeping track of important details in one place.

- Upload Financial Aid Letters: Quickly upload or snap a photo of financial aid awards. Our app reads and standardizes the information for you.

- Factor in Your Resources: Enter 529 plans, scholarships, or gifts to get a full picture of how you can pay for each college.

- Compare Costs: Pick up to four schools to see estimated costs—including tuition, fees, and aid—so you can see an estimated cost of what you’d really pay.

- If you have a funding gap, Award Advisor can introduce you to nonprofit lenders, like VSAC, that offer low-cost student and parent loans.

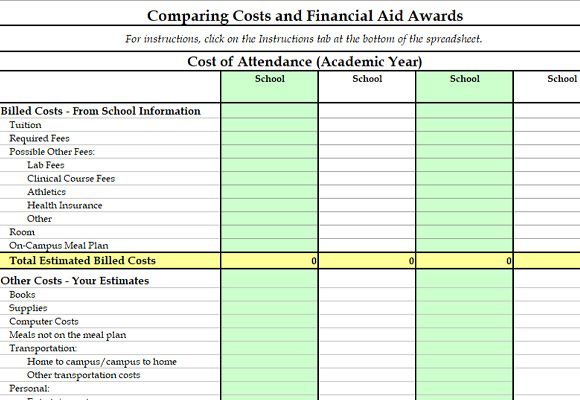

Option 2: Use our Financial Aid Comparison Tool. If you prefer to enter your data manually, we’ve created a simple spreadsheet to help you understand what additional amounts you may need to pay out-of-pocket. If you prefer a more hands-on approach, this simple spreadsheet offers a low-tech way to compare costs and estimate what you may need to pay out of pocket.

3. Making your decision

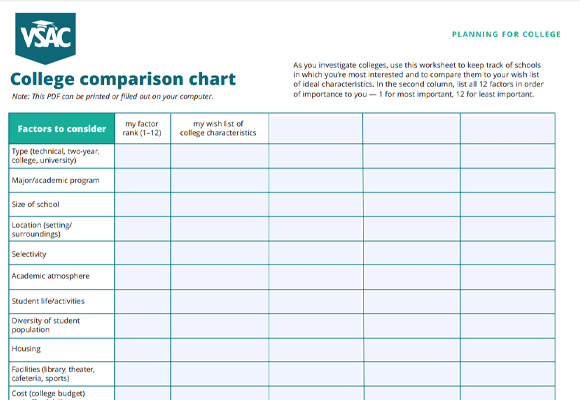

Choosing the right college for you takes a lot of thought. It isn’t just the cost but also the distance from home, major and program options, career services, extracurricular activities, class sizes, student body, and the type of campus environment (school size, city style) you want to experience while studying.

While you're prioritizing your perfect college or career training wish list, use our College Comparison Chart to start considering what matters to you while in school. And once you’re ready to choose, the next journey in your life begins!

Downloadable resources:

Understand Your Offers

Once you have acceptance letters in hand, keep an eye out for emails or snail mail containing financial aid offers from each school. These offers are based on the details you provided on your FAFSA and other financial forms the school might have requested.

Each school will provide a breakdown of the cost of attendance (COA) and the financial aid available to cover the total cost of your education.

Expect each offer to be unique since each school has its own financial aid policies and ways of distributing funds. For example, you might notice differences in the money offered, and differences in the language used to describe grants and loans. There's a lot to consider when making your final choice. But we'll make it easier.

Breaking down the language

There's no one-size-fits-all for these financial aid offers, so don't be surprised or worried by the layout, numbers, or terms used. Although different schools will use different terms, most financial aid offers include some or all of the following:

The one thing they'll have in common is that they may include any or all of the following:

- Grants: free money provided by colleges, state agencies, and the U.S. Department of Education

- Scholarships: student aid offered by different groups, organizations, and even individuals

- Loans: borrowed money that you'll need to repay with interest

- Work-study: an on-campus job that requires a certain number of hours each semester. (To be considered, you’ll have to choose work-study as an aid option when filing your FAFSA.)

You’re not alone if you find it hard to interpret your offer. That’s where VSAC comes in. You can view or download our financial aid vocabulary (PDF) to become more confident when reading your offers. And if you still have questions, you can contact VSAC and we can go through the offer together.

WHAT'S MERIT AID?

Merit aid is free money from a school. It isn't based on financial need. Instead, it is given to students who have academic, athletic, or artistic skills. It could also be given to students who meet certain traits that the school is looking for.

Understand the differences in your offers

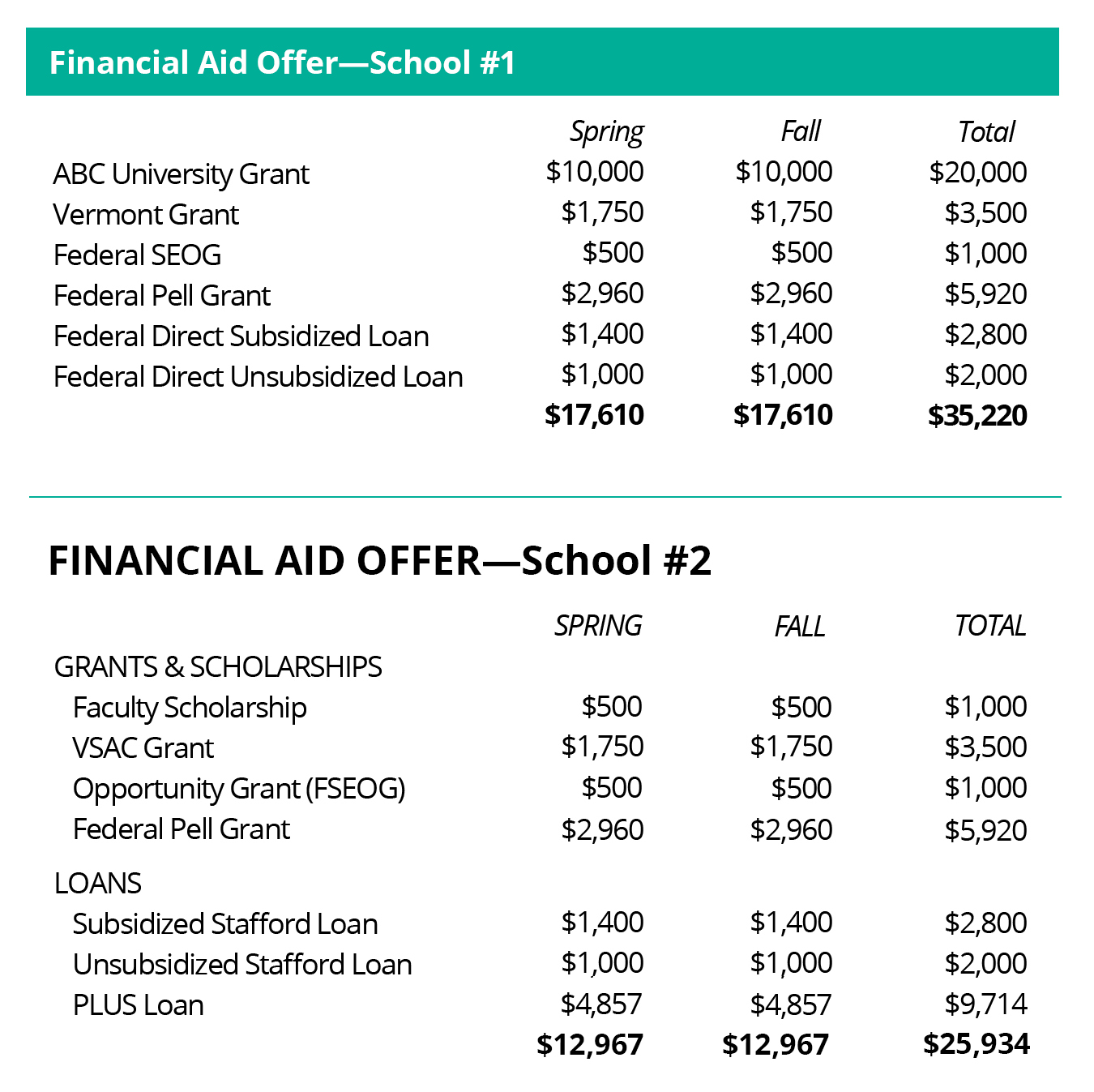

It’s unlikely that you’ll receive two financial aid offers that are exactly alike. Two of the most common areas that create confusion: the differences in how schools describe their free aid and student loans.

You might see this listed as the:

- Vermont grant (because the money comes from the Vermont Legislature)

- VSAC grant (because VSAC administers the grant and students must apply for it through VSAC)

- Incentive grant (the name of the specific grant for full-time students)

These aren't 3 different grants; they're just 3 different ways that schools might refer to Vermont's state grant.

You might also see different names for student (and parent) loans. Loan program names have changed many times over the years, and each school’s language for referencing federal loans is often inconsistent. Just know that:

- Student loans are currently called Federal Direct loans and may appear as DL Sub, DL unsub, Direct Loan – unsub, sub.

- Schools might list loans as Stafford loans.

- You might even see them listed as Ford loans.

- PLUS loans are federal loans typically taken out in the parent's name.

If you have any questions about the types of aid on your financial aid offer, call the school's financial aid office to get more clarity. If you’re still confused, contact VSAC so we can work together to answer any lingering questions.

Spot the differences

In the two examples here, the same state grant is listed with different names (Vermont grant and VSAC grant). The federal loans are also the same, even though the first offer calls them Direct loans and the second offer calls them Stafford loans.

Can you spot another difference in the way the 2 examples refer to the same federal grant?

Listen to VPR’s Navigating College Financial Aid Letters podcast featuring a review of 4 college acceptance offers

Federal Direct Loan vs PLUS Loan

Federal Direct loans are offered by the U.S. Department of Education to eligible students and parents to help cover the cost of college or career training. These loans come with fixed interest rates and flexible repayment options. There are three main types of Federal Direct Loans:

1. Direct Subsidized Loans: These loans are available to undergraduate students whose FAFSA application shows they require additional financial support. The U.S. government pays the interest on these loans while the student is in school at least half-time. They also cover the interest during the grace period after leaving school, and during deferment periods.

2. Direct Unsubsidized Loans: These loans are available to undergraduate and graduate students, regardless of their financial status. Unlike subsidized loans, the student is always responsible for paying the interest on unsubsidized loans.

For both loans, students are the sole borrower and responsible for repayment. For all loan offers, you aren’t required to borrow the full amount. We suggest families only borrow what they need.

3. Direct PLUS Loans: This is a loan for parents of students. The parent is the only borrower for PLUS loans and the loan cannot be transferred to the student.

Like the Direct Unsubsidized Loans, interest will accrue interest once the money is sent to the school.

Parents, it’s your choice whether or not to borrow some or all of the amount offered. Federal PLUS loans have flexible repayment options, such as deferment during periods of hardship. PLUS loans interest rates may also be higher than available alternatives, unlike federal Direct loans for students.

Before borrowing the PLUS loan, pause and shop around for a loan with the best rate and other benefits for your situation. Compare VSAC’s latest loan rates compared to common competitors.

Do you qualify for a PLUS loan?

If your student is offered a PLUS loan, you as the parent will need to submit a separate application in order to determine whether you're eligible. If, as a parent, you're denied a PLUS loan, your student may receive an additional amount of a federal Direct loans.

Once you’ve separated free aid from loans, it’s time to crunch the numbers and get the full picture of your financial aid offers, along with your potential costs. This will help you identify the school that gives you the best deal.

Crunch the Numbers

Once you've looked through your offers to separate the free money from the loans, you'll want to start looking at your bottom line. Take these steps for each school to give you a consistent view of each school's bottom line.

We recommend using Award Advisor™, a spreadsheet, or the online tool to help you make your comparisons. Get our free Award Advisor™ app here or check out our simple financial aid comparison tool.

Step 1: Add up your total college costs

These include not just the tuition and fees, but also room and board, transportation, books, and personal items for the year. This will give you a starting point. If the information isn’t listed in your offer, go online or call the financial aid office to ask for those figures.

Step 2: Subtract your total in "free money"

Next, for each school add up the grants, scholarships, and merit aid—the free money that you don’t have to repay.

Then subtract this amount from the total cost of attendance (for one year) from Step 1.

Contact each school to clarify whether the grants and scholarships will automatically be renewed each year, or if you’ll need to reapply. (Note: Schools require you to fill out a new FAFSA each year you're in school.)

Step 3: Calculate the remaining amount

For each school, the balance between Step 1 and Step 2 is the amount you'll need for 1 year and is the amount you or your family will need to pay from available resources—including savings, current income, and loans.

This balance is your bottom line for each school and the best way to compare affordability.

And remember, this is for 1 year of college. For your total cost, you'll need to multiply this figure by the number of years needed for your degree.

Now that you've identified the net price for each school, you'll need to consider all of the factors that go into choosing the school that's best for your family's situation and your education goals.

Make Your Decision

Choosing the right college takes a lot of thought. It isn’t just the cost but also the distance from home, your major and program options, and the type of environment (school size, class sizes, city style) you want to experience while studying.

While you're prioritizing your perfect college or career training wish list, use our College Comparison Chart to start considering what matters to you while in school.

Compare your options

Start by comparing each school’s total cost of attendance (Line 33 in our college comparison tool). If you’ve filled out the entire sheet, row 64 should display the estimated amount your family is expected to pay for each school. Now that you have the numbers, ask yourself these questions:

- Is there a school that offers the best price?

- Does the cost and what that school offers match up to your wish list?

- How much is the difference between your favorite school and the school that offers the best price?

- How long is each financial aid offer valid? One semester or one year?

Two other important questions to consider are which schools are offering you student loans as part of the package, and how much are the loans going to cost you? Since student loans need to be repaid, preparing for those upcoming monthly payments should be on your mind.

Loans should always be the last option to cover your education costs. And if paying out of pocket is your last option for covering those final costs, you're probably going to need a student loan. VSAC’s free My Education Loans guide offers education to students and families so they know their responsibilities when taking out a loan.

Some things to consider when choosing a college

Keep in mind that financial aid packages will probably change yearly. Sometimes that’s a good thing, especially if you’re getting good grades and creating new opportunities to receive additional scholarships and grants. Other times, even with good grades and new connections, you may still need a loan. Part of the education experience is opening new doors, so that as you invest more time into college and career training, you’ll need to borrow less down the road.

If you’re ever uncertain about the length of your student aid offers or want to know the requirements for eligibility once you're enrolled, call the financial aid office for more details.

Additional Considerations:

- Most financial aid is for only 1 year, so filing your FAFSA yearly is necessary and important. Since federal aid changes yearly, filing a FAFSA yearly can open more opportunities for free aid that reduces your overall cost of education.

- If you’re offered a scholarship, find out if it’s only for 1 year or if it automatically renews each year you’re enrolled.

- Changes in your family’s financial situation can also affect your cost of attendance. If your family income is reduced the next school year or you fall under new financial hardships or obligations, you can appeal your financial aid and possibly receive more aid. Likewise, if your family income increases, you may see a decrease in the amount you receive in grants.

- Build in a 3% tuition hike each year you plan to attend.

Also remember it’s never too late to open a VT529 college savings plan to decrease the amount of money you’ll need to borrow from a student loan.

Still can't decide? Talk to people you trust

Although choosing the best school is your decision to make, you don’t have to decide which college is right for you on your own.

- Discuss your options with people you trust: Talk about your choices with your support team (parents, teachers, family, school counselor) to see if they have any advice.

- Talk to those who’ve gone before you: Contact the colleges’ admissions offices and ask if there are alumni in your area who can meet or talk with you over the phone to answer any questions. You can also join the school’s social media page or visit a college review website like Niche to find out what students have to say about each school.

- Take a campus tour: Planning a trip to visit and get a feel for a school’s energy and the campus environment can also make you more confident in your choice.

- Listen to your instincts: There may not be a perfect school fit, but a good fit and the right choice will look different for you compared to friends. After you’ve compared the numbers, made the right phone calls, and spoken to friends and family, listen to your gut.

- Remember: You can always transfer to another school if you no longer feel like your school is a good fit.

Making your college decision official

Once you’ve made your decision, you’ll need to:

- Send your commitment to your college of choice. Be sure to send the following by the school’s deadline (around May 1 for most colleges):

- Your acceptance of their offer

- The required deposit

- A separate acceptance letter for financial aid (if required)

- Any additional forms or required items (be sure to fill out requested paperwork completely)

- Notify the colleges you won’t be attending. It isn't required, but it will allow the school to offer your spot to another student who may be on the waiting list.

- Begin researching loan options. Tuition bills are typically available in July. Your school will handle the financial aid they're offering and will provide instructions for borrowing federal Direct loans.

If you need additional funding after accepting the maximum amount in federal student loans, then it may be time to consider private loans. But don't make loan decisions until you learn about education loan basics.

What's left?

Congratulations! In the past year, you've navigated your way through a very difficult process, and you're now looking forward to a new adventure. There are just a few things to remember on the home stretch:

- Keep up your grades. Your college will see your final high school transcripts, so it’s important to keep doing well through graduation. This is especially important if you have been granted a scholarship with specific grade requirements.

- You’ve got mail. Due to federal privacy rules, college info will come to you, not to your parents. Sign in to your college e-mail account and get in the habit of reading all e-mails.

- Attend orientation. Most colleges offer day- or even week-long programs. Sign up early to get the date or program you want.

- Sign up for work–study if it was included in your financial aid offer (the best jobs go first).